Understanding the risks in art investment

With a nod to Banksy and monkeys

Welcome to the second edition of the Priceless newsletter and a huge thank you to all of you who have subscribed! It really means a lot, and I’m also super grateful to those of you who suggested topics that you’d like me to cover in future newsletters. Please keep them coming – I promise to do my best to get to them all.

I want to start this edition by sharing an art investment story that I heard recently. I’m not always sure whether to share stories about individual art investments – they are just anecdotes, after all – but this is something that happened recently to a friend I’ve known for 20 years.

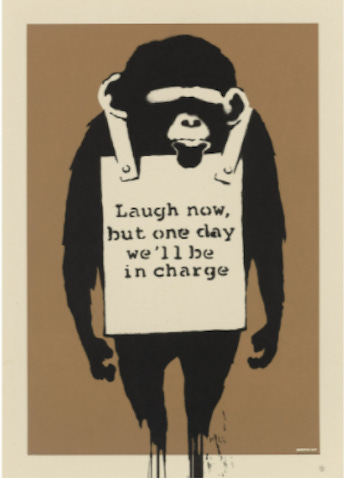

Back in 2003, my friend’s wife bought him Laugh Now, a Banksy screenprint of a monkey wearing a sandwich board with the slogan ‘Laugh now, but one day we’ll be in charge’.

It was for sale for £150 at Santa’s Ghetto, a pop up store for alternative Christmas gifts near London's Carnaby Street, organized by the artist collective Pictures on Walls and billed as “A festive extravaganza of cheap art and related novelty goods from low-brow artists and trained vandals”. It featured works by number of graffiti artists and illustrators, including Banksy and 3D, also known as Robert del Naja, co-founder of the band Massive Attack.

£150 seemed quite a lot for a print, but Banksy murals had been popping up all over Old Street in London where my friend worked at that time, so his wife thought it would make a great present. Plus the print was one of an edition of 150 and signed.

Towards the end of 2020, my friend spoke to a Banksy dealer and told him about the print that he’d had hanging in his house ever since. The dealer said that if he wanted to sell it, my friend’s monkey print was probably worth £150,000.

I nearly fell over when he told me this, particularly because I’m the annoying friend who always tells people to be cautious about art investment. My friend decided not to sell his print because it was a special gift, but if he had, he would have made a 99,900% return on his investment, or a 50.1% compound annual return for 17 years. He now lives in the US and has just had it appraised for insurance purposes for $285,000.

The art market is full of amazing anecdotes like this, which fuels so much interest in art investment. Who wouldn’t want to buy a relatively cheap print, stick it on the wall, and then discover some years later that you could sell it and walk away with the equivalent of $206,000 in your pocket?

His prices have fallen a bit now, but Banksy prints certainly appreciated rapidly in 2020 in spite of, or perhaps because of, his famous anti-art-market stance. The problem is that annual returns across the art market as a whole paint a rather different picture.

The most recent returns for the art market differ depending on which art index you consult, and there is some selection bias in the composition of art indices, which I’ll get to below. However, Art Market Research’s All-Art Index fell 2.1% in the first half of 2021, having increased 71% over the last decade.

Public art sales are currently rebounding, following a big drop after the onset of the pandemic, so full-year returns this year could be better. Even so, the average annual return of Art Market Research’s All-Art Index over the last decade is not very high when you consider that buying art as an investment often comes with risks that are very different to other markets.

This is an issue, because as I pointed out in my last newsletter, there are a growing number of art investment businesses today that suggest investing in art is a straightforward, data-driven business and comparable to investing in other asset classes. So before I start to explore the some of the tools and opportunities available to art buyers, I want to explain these often overlooked risks in more detail to cut through some of the marketing hype.

The art market is opaque

Art indices and most other data resources in the art market are based on records of public art sales at auction – art that has been sold before, otherwise known as the secondary market. These resources are certainly helpful, and I’ll explore them in more detail in a later newsletter, but public auction data is skewed toward the most successful part of the market – the small fraction of artworks that are deemed valuable enough to be resold at auction in the first place.

Public auctions are also not where the majority of art sales take place. Auction sales were $17.6 billion in 2020, which only accounted for about 35% of the estimated $50.1 billion of global art sales that occurred, according to the 2021 Art Basel and UBS art market report:

Global public auction sales, 2011-2020

© Arts Economics (2021)

Private art sales brokered by auction houses made up another 6.3%, while the majority of global art sales (nearly 60%) occurred through private galleries and dealers.

So although investors have access to secondary market data from public art auctions, more than half of the art market’s data is missing – from the completely opaque world of private galleries and dealers. This includes the galleries and other venues where artworks are sold for the first time, also known as the primary market. In this opaque part of the market, it is art dealers who control supply and set prices, which gives those dealers, not investors, access to the most comprehensive art market information.

Some companies are trying to shed light on the opaque part of the market. For example, Artnet and Artfacts have a new partnership that combines Artnet’s secondary market database of auction records with Artfact’s primary market database of exhibition records.

However, auction houses are also selling an increasing amount of art through private transactions, not just public auctions. These private art sales brokered through auction houses were up 36% in 2020 over 2019, according to the Art Basel and UBS report, so in other ways, the opaque part of the market is only getting bigger.

Art prices are subjective

No one wants to overpay for an investment or sell for a discount, and if you are interested in buying or selling a specific artwork, art market indices can give you a good idea of what comparable works have sold for previously. However, public auction prices are influenced by so many subjective factors that nothing is guaranteed.

For example, was any given auction price the result of third-party guarantors bidding up an artwork in which they had a financial interest? Was a buyer willing to pay three times what they thought they should pay for an artwork because it completed their collection? On the flip side, did the auctioneer maintain the momentum throughout the sale, or did half the potential bidders leave for dinner before the last 20 lots were sold, depressing some of the results?

In addition, with the exception of prints and multiples, no two artworks are exactly the same, and even ostensibly similar works can sell for very different prices, even at the very top of the market.

When Sotheby’s sold Basquiat’s Versus Medici in May, a seven-foot tall painting of a warrior figure from Basquiat’s peak year of 1982, its pre-sale estimate was $35 to $50 million. Across town the very same week, Christie’s was selling In This Case, a 6.5-foot skull painting Basquiat completed in 1983. Its pre-sale estimate, although not published, was also around $50 million. In the end, Versus Medici sold for $50.8 million, while In This Case sold for $93.1 million.

The art market is unregulated

Unlike securities and real estate purchases, which generate a mandatory paper trail, information about buyers, sellers, transaction amounts and profits in the art world is not available to regulators, let alone investors – in the US, at least. The opacity of the art market not only makes it a potential conduit for money laundering and fraud, but hard for investors to determine any potential conflicts of interest of buyers or sellers.

The EU and the UK have both recently introduced anti-money laundering rules for the art market, while in the US, regulators are considering whether to use the Bank Secrecy Act, which has already been extended to the antiquities market, to tackle money laundering in the broader art market too. However, even these tighter rules would not make information about buyers and sellers publicly available. One of the promises of NFTs is that they will make the chain of art ownership clear, but that’s not the current reality for all NFT art, let alone the rest of the market.

The art market is illiquid

It’s hard to estimate turnover in the art market, because of the amount of private transactions, but the most recent estimates suggest it’s pretty low. The Art Basel and UBS report estimated that global sales of art and antiquities were $50.1 billion in 2020. By contrast, the average trading volume of Apple shares is currently $11.2 billion a day.

Unlike the stock market, where you can sell shares immediately any time the market’s open, even commercially valuable art can take months or more to sell through a dealer, auction house or other venue, and you are not guaranteed to find a buyer at all. As I discussed in my last newsletter, financial value in the art market is also concentrated around a pretty small number of artists, so it’s hard to know whether most art will go up in value if you do sell it. As an art adviser once told me, 90% of art devalues the minute you leave the gallery with it, and bear in mind that buying and selling art can involve pretty steep transaction costs, plus ownership costs, such as insurance.

So having laid out all the potential pitfalls, how do you acquire art that could appreciate, other than getting insanely lucky like my friend? The next newsletter will start to explore some of the tools and services that can help you navigate this market. If you’d like to read more, I’d love it if you could subscribe, if you haven’t already, and share this with others. It’s free and I’ll do my very best to keep it interesting. Finally, if you’d like to make a small donation to support my work, I’d be very grateful, and you can do so through buymeacoffee.com. Just click on the button below.

I’ll leave you with my picks of the top art investment news of the last quarter. Until next time!

Interpol has launched an app so you can see if the artwork you’re about to buy was ever registered as stolen. Collectors can use the app to upload or take a photo of any artwork and check it against the 52,000 items in Interpol’s Stolen Works of Art database.

LiveArt has launched a peer-to-peer trading platform for art collectors, with the goal of increasing liquidity and cutting transaction costs. LiveArt also offers a valuation service, based on historical auction records and AI-selected similar sales.

Artnet and Artfacts have a new art sales data partnership. See above.

ArtTactic’s latest NFT Market Update reports that the value of NFT sales on Nifty Gateway dropped to $9.6 million in June, from a high of $154.5 million in March.

ArtTactic also released a new report last week that found that auction sales at Christie’s, Sotheby’s and Phillips in the first six months of 2021 now exceed pre-pandemic levels.